How Many Types of Bank Accounts in India

F

Discover verified facts, data, and insights about India’s states, culture, economy, education, and more — all in one place at FactBharat.

Search for a command to run...

Discover verified facts, data, and insights about India’s states, culture, economy, education, and more — all in one place at FactBharat.

No comments yet. Be the first to comment.

Moving to the USA from India is a dream for many. Whether you want to study, work, or live with family, the process can seem complex. But with the right information, you can plan your move confidently. I’ll guide you through the key steps and options...

Opening a college in India is a dream for many educators and entrepreneurs who want to contribute to the country’s education sector. If you are one of those who want to start a college, you need to understand the process clearly. It involves several ...

Opening a hospital in India is a significant and rewarding venture. If you’ve ever wondered how to start one, you’re in the right place. Whether you’re a healthcare professional, entrepreneur, or investor, understanding the process is crucial. You’ll...

Opening a medical store in India can be a rewarding business opportunity. You get to serve your community by providing essential medicines and healthcare products. If you are thinking about starting a medical store, you might wonder where to begin an...

Opening a restaurant in India can be an exciting and rewarding venture. Whether you dream of serving traditional Indian dishes or international cuisine, the process involves careful planning and understanding of local regulations. If you’re ready to ...

FactBharat | Insights About India

2558 posts

Discover verified facts, data, and insights about India’s states, culture, economy, education, and more — all in one place at FactBharat.

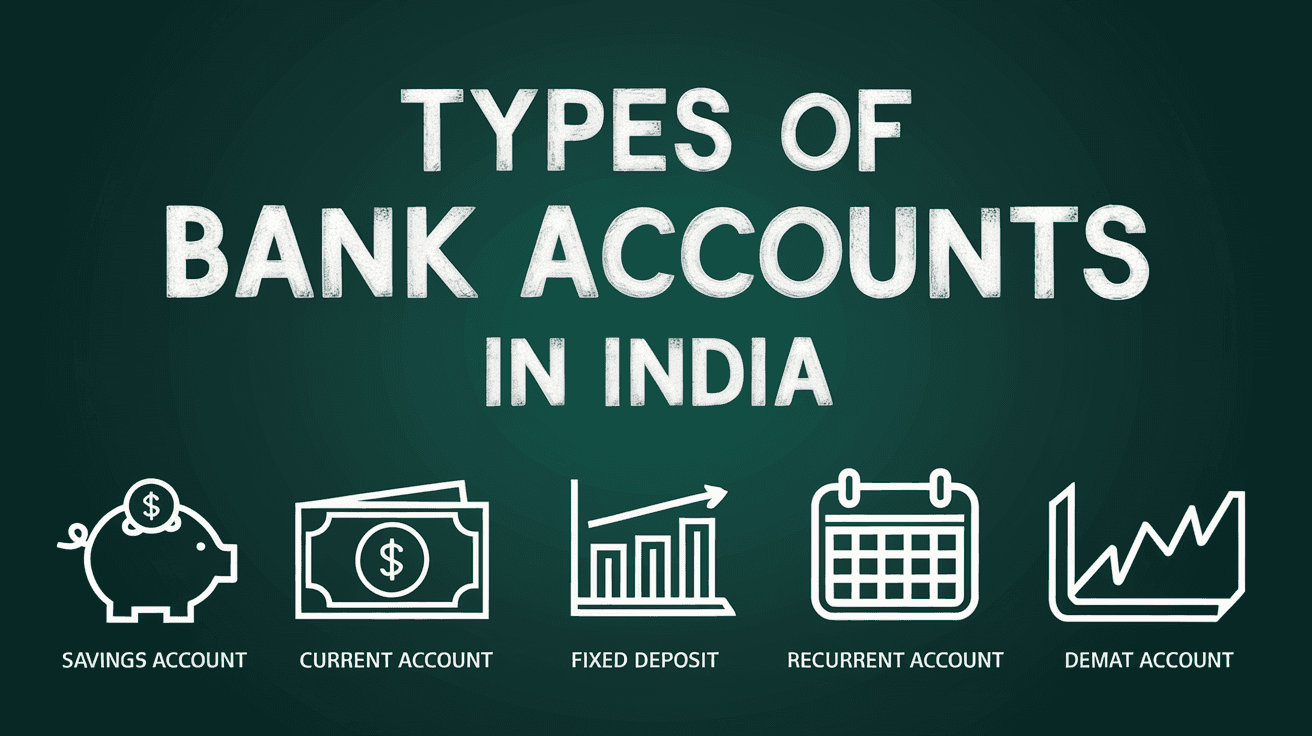

When you think about managing your money, the first step is often opening a bank account. But did you know there are several types of bank accounts in India? Each type serves a different purpose and suits different financial needs. Whether you want to save money, run a business, or invest for the future, knowing the right account type can help you make smarter financial decisions.

In this article, I’ll walk you through the main types of bank accounts in India. You’ll learn what makes each account unique, who should open them, and how they can benefit you. By the end, you’ll be able to choose the best account type for your personal or business needs with confidence.

India’s banking system offers a variety of accounts to meet the diverse needs of its population. Here are the most common types you’ll come across:

A savings account is the most popular type of bank account in India. It is designed for individuals who want to save money while earning interest. This account encourages saving habits and provides easy access to your funds.

Savings accounts are flexible and allow you to deposit or withdraw money anytime. They are also linked to various digital payment platforms, making transactions easier.

Current accounts are mainly for businesses, traders, and professionals who need to handle frequent transactions. Unlike savings accounts, current accounts do not usually earn interest.

Current accounts help businesses manage their daily cash flow efficiently. They offer features like overdraft, which allows you to withdraw more than your balance up to a limit.

A fixed deposit account is a term deposit where you lock your money for a fixed period at a predetermined interest rate. It is a safe investment option with higher returns than savings accounts.

FDs are popular because they offer guaranteed returns and help in financial planning. You can choose the tenure based on your financial goals.

A recurring deposit account lets you save a fixed amount every month for a specific period. It is a disciplined way to save regularly and earn interest.

RDs are great for those who want to save small amounts consistently and earn interest on their savings.

Non-Resident Indians (NRIs) have special bank accounts tailored to their needs. These accounts help NRIs manage their income and investments in India.

Each NRI account serves different purposes, such as managing foreign income or Indian earnings.

The government introduced BSBDA to promote financial inclusion. It is a zero-balance account with limited services but no minimum balance requirement.

BSBDA helps bring more people into the formal banking system, especially in rural areas.

Apart from the common types, there are some specialized accounts designed for specific groups or purposes.

Banks offer special savings accounts for senior citizens with higher interest rates and additional benefits.

These accounts provide financial security and convenience for senior citizens.

A salary account is a type of savings account where your employer directly deposits your salary. It often comes with zero minimum balance and additional benefits.

Salary accounts simplify salary management and often come with perks like easy loan approvals.

Parents or guardians can open accounts for minors to help them learn about saving money early.

Minor accounts teach financial discipline and help build savings from a young age.

Choosing the right bank account depends on your financial goals and needs. Here are some tips to help you decide:

For example, if you want to save money regularly, a savings or recurring deposit account is ideal. If you run a business, a current account suits your needs better.

Having the right bank account can make managing your money easier and more rewarding. Here’s how:

Choosing the right account helps you avoid unnecessary fees and maximize your financial benefits.

Understanding how many types of bank accounts are available in India helps you make informed financial decisions. From savings and current accounts to fixed and recurring deposits, each type serves a unique purpose. Whether you are an individual, business owner, or NRI, there’s an account tailored for your needs.

By knowing the features and benefits of each account, you can pick the one that fits your lifestyle and goals. Remember to consider factors like interest rates, minimum balance, and transaction needs before opening an account. With the right bank account, managing your money becomes simpler and more effective.

There are mainly six types: savings account, current account, fixed deposit, recurring deposit, NRI accounts, and basic savings bank deposit accounts.

Savings accounts earn interest and are for individuals, while current accounts are for businesses and do not usually earn interest but allow frequent transactions.

Yes, minors can have accounts operated by their guardians, designed to teach them saving habits.

A fixed deposit is a term deposit where money is locked for a fixed period at a higher interest rate than savings accounts.

Yes, senior citizen accounts offer higher interest rates and additional benefits like free health check-ups.